When Age Changes but Power Doesn't

Bloomberg says CEO age is rising. But age is just the easiest variable to narrate as change. Gender tells the harder story: power remains overwhelmingly male.

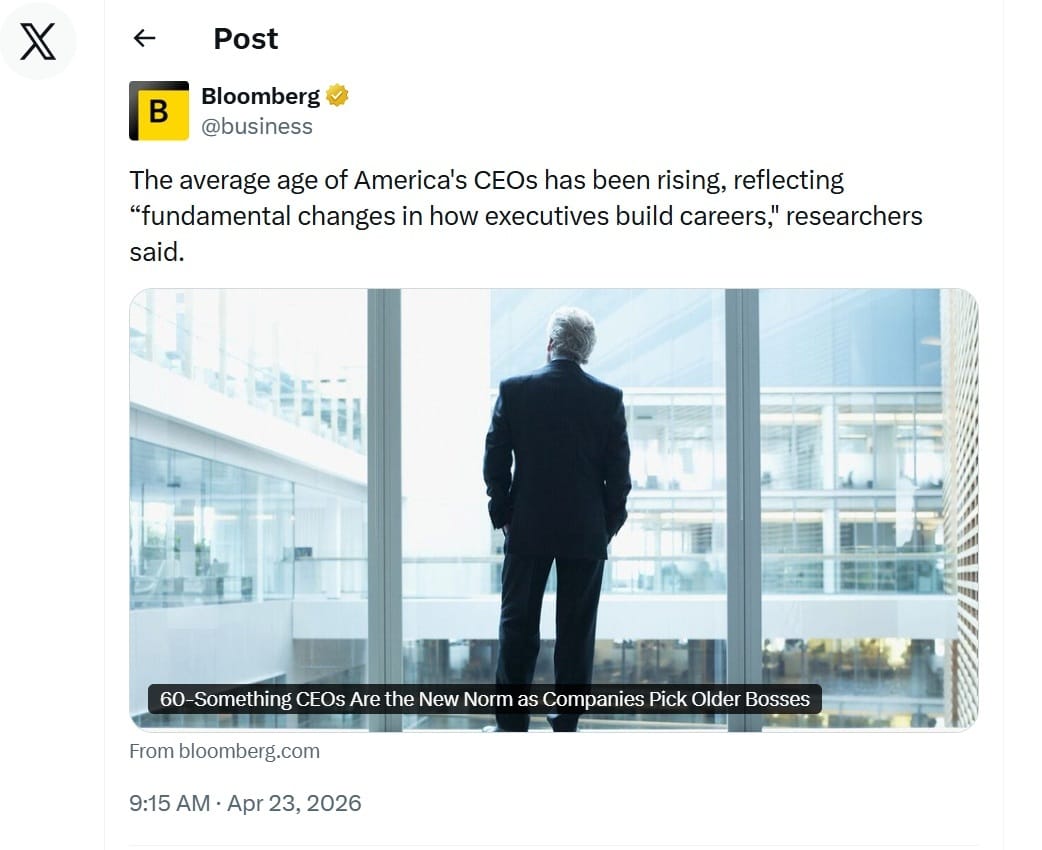

Bloomberg says the average age of America’s CEOs has risen, calling it a “fundamental” change in how executives build careers.

The supposedly sweeping change is this: the most likely age of Fortune 500 CEOs rose from about 58.5 to 61.

That is all. 2.5 years change in CEO age over a quarter century.

I am underwhelmed.

What has changed far less is the gender makeup of Fortune 500 CEOs.

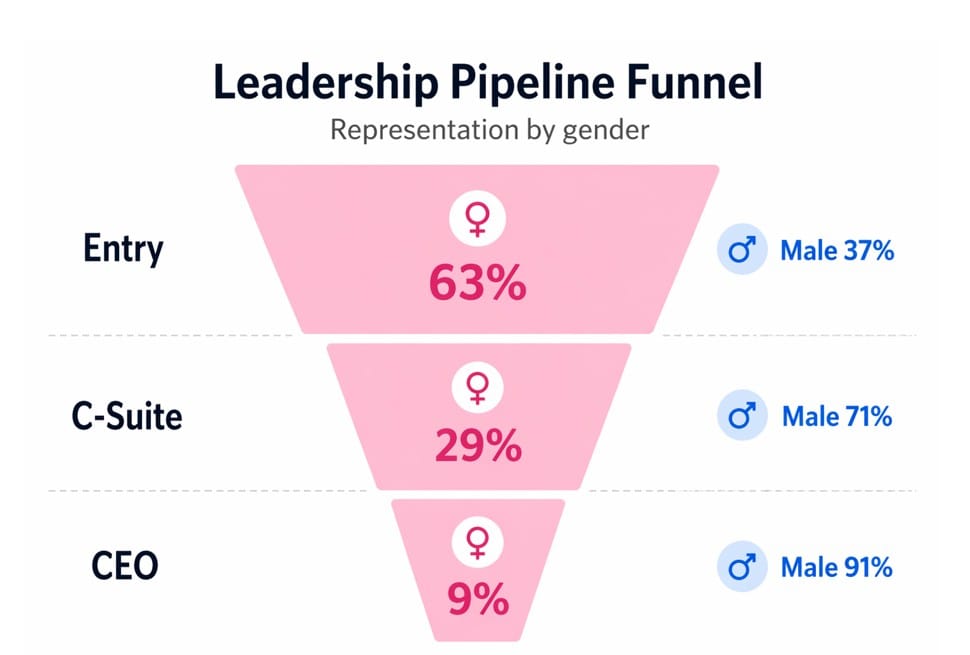

At the entry level, office workers are now majority female, about 63 percent in the U.S. By the C-suite, that narrows to 29 percent. At the Fortune 500 CEO level, it narrows again, to just 9 percent.

So yes, CEOs are getting ever-so-slightly older.

Fortune 500 CEO Ages 2015-2026

| Year | Average CEO Age | Median CEO Age |

| 2015 | 58.2 | 58.5 |

| 2016 | 58.5 | 58.8 |

| 2017 | 58.9 | 59.1 |

| 2018 | 59.2 | 59.3 |

| 2019 | 59.6 | 59.5 |

| 2020 | 60.1 | 59.8 |

| 2021 | 60.4 | 60 |

| 2022 | 60.8 | 60.2 |

| 2023 | 61.3 | 60.4 |

| 2024 | 61.7 | 60.6 |

| 2025 | 62.1 | 60.8 |

| 2026 | 62.5 | 61 |

They are also still overwhelmingly male.

The Promotion Gap

I was sold a story about the lack of supply.

In my 20s, the standard explanation for skewed CEO rosters was that there simply were not enough women entering the workforce. That excuse no longer holds. Women have been near parity or majority in office work for decades and now make up 63% of entering office workers. The narrowing happens later.

For every 100 men promoted to manager, only 93 women are promoted, and only 74 women of color. The gap continues at every successive rank. By the time the pipeline reaches enterprise leadership, the field has already materially narrowed.

How CEOs Are Actually Chosen

Boards do not pick a CEO in a vacuum.

They choose a candidate they believe will look credible to the people who hold capital, price risk, and react to appointments.

That is where the filter hardens.

In venture capital, hedge funds, and private equity, the gender skew remains extreme. As of early 2025, women held only fifteen percent of decision-making roles at VC firms. In hedge funds, the share of women in senior portfolio management is smaller still, at twelve percent.

At the board level, women have gained some representation overall, but the roles that actually shape the shortlist, chair positions and nomination committees, remain disproportionately male.

Then comes homophily, the ordinary tendency of people to trust and elevate those who resemble themselves. When a board composed mainly of older men looks at a fund manager or operating executive who is also an older man, the conclusion often arrives before it is articulated: he looks like a CEO, just my type of fellow.

Investor reaction reinforces the same pattern. In 2025, research found that analysts and investors reacted less to earnings forecasts issued by female CEOs than to identical forecasts issued by male CEOs. The numbers may be the same, however the female voice is treated as less credible by the market.

Boards notice this. They fear a stock-price dip. If they believe, rightly or wrongly, that the market will greet a female appointment with skepticism, they will often choose the supposedly safer male candidate and call it prudence.

Finally, they invoke the experience screen. Prior CEO experience. Enterprise-scale P&L responsibility. Ten years in the "right" feeder roles. Because women have historically been blocked from precisely those assignments, the board can say, with a straight face, that it would have loved to hire a woman, but none of the candidates had the required track record.

That is how exclusion gets laundered into process.

The Finance Glacier

The same pattern appears in finance itself.

Named fund managers and portfolio managers have not meaningfully diversified. According to Morningstar and related industry data, women’s representation here has actually regressed, from roughly 13 to 14 percent in the early 2000s to merely 11 percent in 2026.

In wealth management, women remain clustered more heavily in administrative and operational roles than in the revenue-producing seats that build capital credibility and feed later leadership selection.

So the investment side and the operating side are not telling different stories.

They are telling the same story.

What Actually Changed

The Bloomberg framing is revealing, though perhaps not in the way intended.

Age is easy to narrate as transformation. It is safe and shows supposed "progress" into selection by greater levels of experience. A few extra years on the average CEO can be described as a “fundamental” shift in how careers are built.

Gender is harder to narrate that way, because it forces the more uncomfortable conclusion: the selector class has changed far less than the headline suggests.

The pipeline is not empty of women. It is narrowed.

The boardroom is not neutral. It is filtered.

The market is not purely rational. It is credence-sensitive.

So the visible outcome is predictable.

Age drifts upward. Male control stays sticky.

And when women lose ground, as we have over the last two years, no headlines are written about it.

For the CST Practitioner

This is not just a diversity story. It is a systems story.

A system can absorb meager change in a visible variable, age, and then narrate that movement as "proof of transformation" while the deeper power variable remains largely intact.

That is one form of institutional misdirection.

The question is never only, What changed?

It is also, What changed because it was easy to change, while something more load-bearing stayed the same?

— Madonna Demir, founder of Convivial Systems Theory and author of Systems & Soul

GenZ refuses workplace theater expectations in this next Systems-in-Action piece